🔬 Your Monthly Alpha Lab Deep Dive

A mean-reversion strategy that buys recent losers among large-cap stocks, expecting short-term price corrections to generate alpha.

Welcome to your monthly Alpha Lab deep dive.

At the end of each month, you’ll get a deep dive featuring Python code to backtest and analyze a live trading strategy. Remember, you can also drive the conversation and support topics your way. Create new threads to start conversations about the code, strategies, and topics you care about.

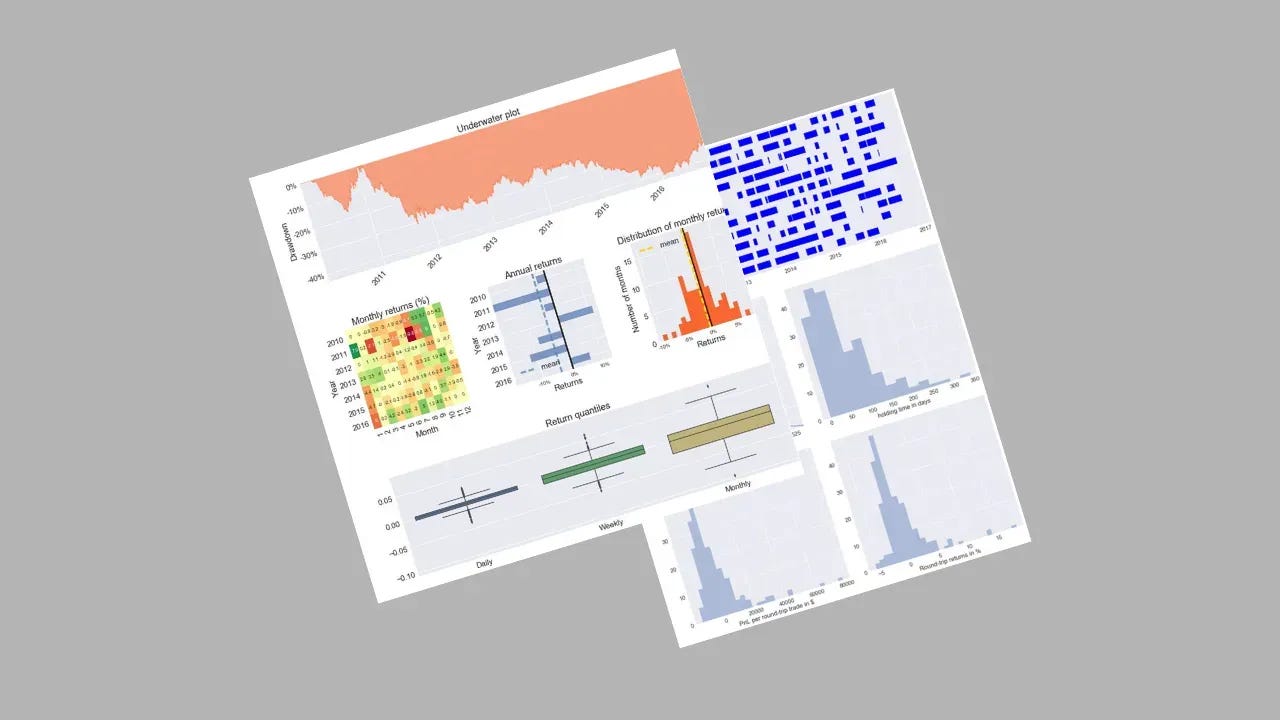

In this month’s deep dive inside PyQuant News Alpha Lab, you’ll build and backtest a classic anomaly-driven strategy: Short-Term Reversal in Stocks.

The idea is simple but powerful—identify recent losers among large-cap US stocks, then buy the worst performers from the past week with the expectation that short-term overreactions will correct. The strategy selects the 30 worst-performing stocks from the top 100 large-cap universe, weights positions using inverse volatility, and rebalances weekly to capture the short-term reversal premium.

You’ll also walk through the full workflow in Zipline, including universe selection, custom factor creation, volatility-based position sizing, realistic commission and slippage modeling, weekly rebalancing logic, and long-term performance analysis. By focusing on large-cap stocks and using inverse volatility weighting, the strategy aims to reduce transaction costs, improve portfolio stability, and make the reversal effect more practical to test.

By the end, you’ll have a complete backtest, from factor creation to backtest execution, plus performance evaluation using CAGR, Sharpe ratio, annualized volatility, and max drawdown.